Support from readers like you keeps The Journal open.

You are visiting us because we have something you value. Independent, unbiased news that tells the truth. Advertising revenue goes some way to support our mission, but this year it has not been enough.

If you've seen value in our reporting, please contribute what you can, so we can continue to produce accurate and meaningful journalism. For everyone who needs it.

AN EU DIRECTIVE requires Ireland to oblige non-entity banks and credit purchasers to start offering forbearance to mortgage holders, Master of the High Court Edmund Honohan has told an Oireachtas committee.

Speaking to committee members today, he said the public have a right to be informed about the EU Directive on Credit Servicers and Credit Purchasers, which contains new guidelines for forbearance, including, where possible, partial debt forgiveness.

The Europe-wide process for dealing with mortgage indebtedness is due to be signed into Irish law by 29 December of this year.

EU member states have an element of discretion in terms of transposing the directive, but Honohan states Ireland should transpose it in full.

The directive sets out that EU Member States should have appropriate forbearance measures in place at national level.

When deciding which forbearance measures to take, creditors should take into account the individual circumstances of the consumer, the interest rate they are paying and the ability to repay, it states.

The directive sets out that forbearance measures should be able to consist of certain concessions to the consumer, “such as a total or partial refinancing of a credit agreement, or a modification of its existing terms and conditions”, which includes:

the extension of the loan term

a change of the type of credit agreement

a deferral of payment of all or part of the instalment repayment for a period

a change of interest rate

an offer of a payment holiday

partial repayments, currency conversions

partial forgiveness and debt consolidation.

Advertisement

Non-bank entities hold around 112,000 mortgages in Ireland, many of which were sold on from retail banks.

While the perception is that these are non-performing loans in arrears, the committee was told that is not the case with many mortgage holders having never missed a payment with their commercial bank before being sold on.

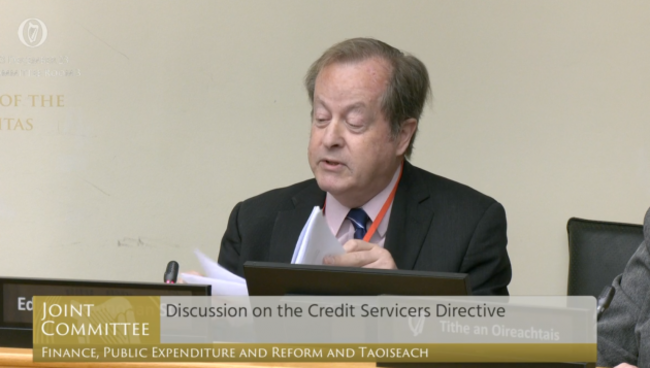

Edmund Honohan at the Oireachtas Finance Committee today.

The purpose of the directive is to promote a governing framework and provide for a new EU wide authorisation for credit servicers to be overseen by national competent authorities, which in Ireland’s case will be the Central Bank.

Honohan said it is a “bit of good news” that should be put out there, in the hope that it can get “enough momentum behind it” that mortgage holders who are in distress in the run up to Christmas “would stay the course”.

He told the committee that his chief concern with the new EU directive is that judges will not know the detail of the new legal position it creates.

There is an “information deficit in how judges are operating now”, he said, stating that it shouldn’t fall on the lay person to have to explain the new position to the courts.

It is his concern that the changes “will not be picked up on”, he stated.

Honohan said an “obligation arises now on the Central Bank in keeping the public informed on forbearance”.

Related Reads

Minister calls on Pepper to be 'absolutely clear' with customers about new fixed mortgage interest rate

McGrath tells banks and vulture funds to outline supports for mortgage holders trapped with high interest rates

'They got away with it for too long': Harris won't thank bankers for upping saving interest rates

Describing it as a significant change in the law, it specifically mentions debt forgiveness, he told committee members.

Sinn Féin’s Pearse Doherty and other committee members said they had been dealing with a multitude of cases of people having their loans and mortgages sold on to non-entity banks.

Fianna Fáil’s John McGuinness said he knows many families who have had their lives destroyed dealing with vulture funds and credit servicers, stating that he hoped this new framework would make a difference.

One of the “great benefits” of the directive, is it states that forbearance should happen before court proceedings commence, said Honohan.

Doherty asked if it is is Honohan’s view that a reasonable offer from a lender cannot be classed as reasonable offer if it doesn’t offer partial forgiveness, as set out in the directive.

“Yes, that is it,” he said.

Honohan said the directive says this system should be in operation and says the state should oblige lenders to offer forbearance.

“That is hard law, there is no way of getting around that,” he said.

Readers like you are keeping these stories free for everyone...

A mix of advertising and supporting contributions helps keep paywalls away from valuable information like this article.

Over 5,000 readers like you have already stepped up and support us with a monthly payment or a once-off donation.

To embed this post, copy the code below on your site

Close

8 Comments

This is YOUR comments community. Stay civil, stay constructive, stay on topic.

Please familiarise yourself with our comments policy

here

before taking part.

@Tony Gordon: its easy to make it one or the other black or white but turf cutters are trying to heat their homes, if you want it to stop you have to replace the turf with solar or wind attacking turf cutters is beyond counter productive. Same with the carbon tax hitting families in their heating and cars and taking turf cutters to court punishing people while providing no alternative is just torturing people. Anyone who is angry about this should be thinking about a better solution not a way to convict someone trying to heat their homes

@Rúraíocht: the parents of a child can argue the FGM is cultural & traditional, but it’s still wrong and illegal… time for the turf cutters to get with the times.

Everyone is making a sacrifice when it comes to trying to reverse climate change, culture & tradition is just an excuse to be ignorant.

@Matthew O’Kane ☘️✊#BERNIEBEATSTRUMP: good to see someone with common sense commenting on this issue, as for a lot of they other comments, common sense is not that common.

@Tony Gordon: Derrybrien wind farm caused much more destruction to our environment than these men could do in 200 years, when is the trial for the developers? They too broke EU law. 20000 fish killed. Spawning beds ruined.

Well, I cut turf in our bog every year, there are 3 tractor loads, 1 for myself, 1 for my father and my brother gets 1 for himself, this consists of about about 20 lines. However, some people cut it for selling, while thats their choice it needs to stop. We were brougbt up in the bog, good hard work didnt do us any harm, we cut for ourselves and thats it. I do see the destruction it can do, theres no doubt about it. Things have to change and i think they will because the next generation behind us dont want to work at turf.

@Lucille Ball: Agree, the safeguard is the new crew will leave the peat in the ground. Climate change, flooding and infrastructure projects, incl roads, housing, wind turbines are a bigger risk to these ecosystems.

@Lucille Ball: You are just like most Country folks who had a plot of bog, others who had none often rented a bit from a neighbour. That was back when the Slain was in operation and the old wooden barrow. Great times , but hard work, especially if the weather turned bad and there was a lot of handling. The digger and turf machine was a different set up. A lot of them made holes everywhere, made big drains, did a lot of harm really to the natural environment there, they were there to make as much money as possible in a short period, and they were indifferent as to whether the damaged all around them. That changed the whole structure of the bog for the worse.

@Lucille Ball: so turf for you and your family because of your birthright entitlement to it, but not for sale to anyone else because it’s too damaging? You can’t have your cake and eat it too. It’s nothing to do with whether a generation wants to work at turf or not, it’s about protecting an ecosystem and preventing overexploitation of a resource, regardless of tradition

@Brendan Gordon: no Brendan, each to their own, I’m saying I don’t cut turf to sell for profit some do which is their choice, however the more turf that’s cut the more damage there will be

@Lucille Ball: If they cut the same amout to sell as your family does for themselves then what’s the difference? The damage is still being done and that’s why there are protected designations. You are cutting for profit because it’s money you don’t have to spend on other fuels. You can’t act like you’re morally better. Either you act within the law or you don’t

@Brendan Gordon: Jesus are you dim? I cut a trailer load that does me for a year, those that cut turf to sell in my experience can cut up to ten loads for sale and have 1 for themselves.. I do t cut for profit, I cut enough to heat my house for the year. I could cut for profit but I don’t

@Lucille Ball: I also don’t condemn anyone that cuts their bog for profit, I do my own thing and keep my nose out of others business, each to their own

@Lucille Ball: the whole point of environmental campaigning is that it’s not each to their own. By that logic if somebody cut down a rainforest or killed a few whales nobody could have an opinion on it. It’s a shared planet and we all share the natural resources including the generations yet to be born.

@Lucille Ball: No but you obviously are yourself. I specifically said if you cut the same amount. If you didn’t cut you’d have to buy fuel elsewhere so you do profit, but you show restraint to make it last longer. Your neighbors don’t and cut more than you and sell. The outcome is the same, the peat is gone, you just made it last longer, but it’s not going to “grow back”. If it’s ok to cut the turf, what difference does it make who consumes it? If there is laws against extraction, or excessive annual extraction, obey them.

@Lucille Ball: isn’t that how ecosystems disappear? Everyone cuts down their edge of the forest thinking there’s plenty left, till there isn’t any. But fair play for your honesty.

Unreal bringing 4 guys to court over trying to keep there family warm for the winter…

If some people want to give out about family’s cutting turf in a bog why don’t you take a drive down through the Midlands and see who the biggest culprit in the bog is? The state! Cutting away and topping miles and miles of peat bogs to burn in power stations! But you won’t see them being brought to court!

@Damien Tyrrell: 100% right, and look at Irelands shocking performance on latest climate report. Hope the new government makes some real changes re environment.

@john mounsey: I don’t think we are allowed a new government, I think we have to go back to the old one as too many people voted the wrong way. Ah well nevermind, plenty of EU fines on the way.

But they haven’t been vindicated, if it had gone to a full trial and they found not guilty that would be so, but neither were the found guilty. The whole issue of turf cutting remains in limbo until there is a complete trial one way or the other.

As a person with fond memories of footing turf since the 80′s, I cheer the turf cutters. Better for them to take a few sods than the hypocritical and inane use of peat in crazily expensive state power stations.

@john mounsey: “the hypocritical and inane use of peat in crazily expensive state power stations.”

But that’s the whole point isn’t it, the peat fired power stations are a thing of the past because peat is inefficient and has a very high carbon footprint.

Just because something is a tradition does not mean it should continue regardless.

@john mounsey: The famine is history so now we have no need to poach fish. Peat will also become history as we move to more sustainable forms of energy.

There is no good reason to keep burning peat.

@john mounsey: famine is long over. People that poach fish do so out of greed and for profit. Salmon stocks are on the verge of collapse yet poachers operate up and down the country without giving a hoot about the damage they’re doing. The same applies to the bogs, i get the argument about it being a generation thing and all that but the damage it is doing cannot be undone.

“Why is that a protected bog,Daddy “? Because it’s one of the last of its kind in all of Europe, and burning turf is damaging our environment. It is also home to different species of rare animals, birds ,insects and plants. “So why are men digging it up with tractors “? “Because this is Ireland my boy. This is Ireland. “

@Leonard O’mahony: There are plenty of bogs protected so just leave the few working bogs alone. The owners will finish up in time anyway and those of is who worked on saving turf know well that the bog returns to its natural state very quickly once the work ceases.

@Joseph Larkin: returns to what seems like a natural state due to top layer regrowth. It has a growth rate of 1mm per year meaning 1000 years to get 1m deep. I wouldn’t consider that quick

How much turf have bord na mona extracted in eight years? Using machinery bought by taxpayers to harvest hunderds of acres of bogland without any regard for climate change. But customers paid carbon tax on that produc.

This was an attack on rural Irish families by FG and one labour minister. The state can’t take away people’s property rights.

@leartius: You clearly don’t know or understand what goes on. Bord na mona don’t cut turf, private contractors do and they buy their own machines. Turf spread on the bog is also not subject to the carbon tax. When you buy dried turf in a load or bags carbon tax is supposed to be applied but not to wet turf spread on the bog which you save yourself.

It’s not really a great day for rural Ireland, although it was a good outcome for these men.

The cost of the huge carbon emissions associated with turfcutting will have to be paid by others, many of them taxpayers living in rural Ireland.

@John Mulligan: Do you think that the carbon emissions from turf cutting are higher than oil and gas extraction?

With oil and gas you have to drill several wells, this includes 3 support vessels to move the rig and another 2 to supply it each burning 20m3 a day of mgo.

The chopper that goes to the rig daily, the production of drilling mud, brine, cement etc and the mgo the rig is burning.

Then build the Subsea infrastructure and FPSO or platform, get the product ashore, refine it and put it in a tanker. Then it goes in a lorry to your house or is piped in if it’s gas.

Or you have people with a machine that cut the turf and run a tractor for 2 days.

I think the sale of turf should be stopped, but for home use it’s already dying out so just let them at it and it will end naturally.

@Robert Conneely: I think you are absolutely correct it will die out naturally. The amount of private harvesting is minuscule in terms of carbon footprint and peat remains a very cheap source of fuel for many rural dwellers.

As for the damage to the bogs the focus is on the destruction of the natural bog; but it recovers very quickly as any bog owner will testify.

Environmentalists want all bogs left in pristine condition; that’s ok from the comfort of your gas fired central heating but plenty of bogs will remain untouched in rural Ireland while the ones being worked currently will return to their natural state in a matter of years.

@Robert Conneely: I never defended oil and gas, I just pointed out that turf cutting is an incredibly carbon heavy method of heating homes.

‘Whatabout oil’ is diversionary, and it doesn’t solve the problem, or explain who will pay the cost of turf cutting.

@Robert Conneely: it should be confined to people turf cutting for home use under license if necessary. However there are other more pressing areas where carbon footprint could be reduced.

@John Mulligan: But is it really when everything is taken into consideration?

The reason I stated oil and gas is that’s the alternative at the minute, until renewables come online or we go to community based hot water from something like geothermal I can’t see it being worse.

Currently I’m on a very large construction vessel off Ghana burning 50m3 a day and there are another 4 light construction vessels all working around us while the FPSO flares off the gas.

I don’t agree with turf cutting but if peoples houses are cold then thry need to be heated. Lets get old houses up to an A energy rating and there will be no need to cut turf anymore.

@great gael of Eire: a B rating is very warm compared to what’s there and costs a lot less to upgrade to.

A rating requires air tightness measures which cost a fortune.

@Kenneth Finnerty: as opposed to that tax increases we’d need in future to subsidise fuel costs when scarcity drive prices way out of peoples reach? Better to invest in an asset that will pay off than to put it on the back burner and bleed ourselves dry slowly.

@Kenneth Finnerty: The idea is that we work with people. There is a great quote “In the end unless everyone wins, no one wins”. We have a society where one group of people are dictating to another group of people telling them what they can or can do. it doesn’t work. Look at prohibition or the war on drugs. Banning something outright does not work. Give people alternatives.

“Ireland’s raised bogs are the only examples remaining in Western Europe and there is now less than 1% of the original area left in Ireland in good condition” but people are determined to destroy even that too. Hand turf cutting is one thing that could be allowed but heavy machinery is totally destructive and should be banned.

Destroy protected bogs, cut hedges when birds are nesting, shoot Eagles and Osprey, burning gorse during heat waves, let slurry run off into our streams etc. there are some incredibly ignorant people living on this island, true definition of gobshytes.

@Tjamr: also build windfarms like Derrybrien wind farm which caused much more destruction to our environment than these men could do in 200 years, when is the trial for the developers? They too broke EU law. 20000 fish killed. Spawning beds ruined.

Don’t we all love that 1950s John Hinde postcard of two children and a donkey carrying a creel of cut turf? That was the image of innocent Third World Ireland that the Americans cherished. Bord Failte never discouraged it then.

@Garreth Byrne: ugh…. 70 years ago Americans liked it, and the tourism board (nothing to do with turf) didn’t disagree…… What’s this got to do with anything?

Derrybrien wind farm caused much more destruction to our environment than these men could do in 200 years, when is the trial for the developers? They too broke EU law. 20000 fish killed. Spawning beds ruined.

@Braonain Proinseas: there was evidence at the start. I took so long to come to trial and the main witness is now abroad so couldn’t testify. Did you not read the article?

'I presume this is free?' Confusion over when women will get long-awaited free HRT from pharmacies

2 hrs ago

1.1k

19

Heathrow

Heathrow closure: Limited flights resume this evening as fire thought to be 'non-suspicious'

Updated

3 hrs ago

56.3k

97

tiktok

Who is Garron Noone and why are politicians claiming he was 'silenced'?

9 hrs ago

58.0k

Your Cookies. Your Choice.

Cookies help provide our news service while also enabling the advertising needed to fund this work.

We categorise cookies as Necessary, Performance (used to analyse the site performance) and Targeting (used to target advertising which helps us keep this service free).

We and our 160 partners store and access personal data, like browsing data or unique identifiers, on your device. Selecting Accept All enables tracking technologies to support the purposes shown under we and our partners process data to provide. If trackers are disabled, some content and ads you see may not be as relevant to you. You can resurface this menu to change your choices or withdraw consent at any time by clicking the Cookie Preferences link on the bottom of the webpage .Your choices will have effect within our Website. For more details, refer to our Privacy Policy.

We and our vendors process data for the following purposes:

Use precise geolocation data. Actively scan device characteristics for identification. Store and/or access information on a device. Personalised advertising and content, advertising and content measurement, audience research and services development.

Cookies Preference Centre

We process your data to deliver content or advertisements and measure the delivery of such content or advertisements to extract insights about our website. We share this information with our partners on the basis of consent. You may exercise your right to consent, based on a specific purpose below or at a partner level in the link under each purpose. Some vendors may process your data based on their legitimate interests, which does not require your consent. You cannot object to tracking technologies placed to ensure security, prevent fraud, fix errors, or deliver and present advertising and content, and precise geolocation data and active scanning of device characteristics for identification may be used to support this purpose. This exception does not apply to targeted advertising. These choices will be signaled to our vendors participating in the Transparency and Consent Framework.

Manage Consent Preferences

Necessary Cookies

Always Active

These cookies are necessary for the website to function and cannot be switched off in our systems. They are usually only set in response to actions made by you which amount to a request for services, such as setting your privacy preferences, logging in or filling in forms. You can set your browser to block or alert you about these cookies, but some parts of the site will not then work.

Targeting Cookies

These cookies may be set through our site by our advertising partners. They may be used by those companies to build a profile of your interests and show you relevant adverts on other sites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies, you will experience less targeted advertising.

Functional Cookies

These cookies enable the website to provide enhanced functionality and personalisation. They may be set by us or by third party providers whose services we have added to our pages. If you do not allow these cookies then these services may not function properly.

Performance Cookies

These cookies allow us to count visits and traffic sources so we can measure and improve the performance of our site. They help us to know which pages are the most and least popular and see how visitors move around the site. All information these cookies collect is aggregated and therefore anonymous. If you do not allow these cookies we will not be able to monitor our performance.

Store and/or access information on a device 110 partners can use this purpose

Cookies, device or similar online identifiers (e.g. login-based identifiers, randomly assigned identifiers, network based identifiers) together with other information (e.g. browser type and information, language, screen size, supported technologies etc.) can be stored or read on your device to recognise it each time it connects to an app or to a website, for one or several of the purposes presented here.

Personalised advertising and content, advertising and content measurement, audience research and services development 142 partners can use this purpose

Use limited data to select advertising 112 partners can use this purpose

Advertising presented to you on this service can be based on limited data, such as the website or app you are using, your non-precise location, your device type or which content you are (or have been) interacting with (for example, to limit the number of times an ad is presented to you).

Create profiles for personalised advertising 83 partners can use this purpose

Information about your activity on this service (such as forms you submit, content you look at) can be stored and combined with other information about you (for example, information from your previous activity on this service and other websites or apps) or similar users. This is then used to build or improve a profile about you (that might include possible interests and personal aspects). Your profile can be used (also later) to present advertising that appears more relevant based on your possible interests by this and other entities.

Use profiles to select personalised advertising 83 partners can use this purpose

Advertising presented to you on this service can be based on your advertising profiles, which can reflect your activity on this service or other websites or apps (like the forms you submit, content you look at), possible interests and personal aspects.

Create profiles to personalise content 38 partners can use this purpose

Information about your activity on this service (for instance, forms you submit, non-advertising content you look at) can be stored and combined with other information about you (such as your previous activity on this service or other websites or apps) or similar users. This is then used to build or improve a profile about you (which might for example include possible interests and personal aspects). Your profile can be used (also later) to present content that appears more relevant based on your possible interests, such as by adapting the order in which content is shown to you, so that it is even easier for you to find content that matches your interests.

Use profiles to select personalised content 34 partners can use this purpose

Content presented to you on this service can be based on your content personalisation profiles, which can reflect your activity on this or other services (for instance, the forms you submit, content you look at), possible interests and personal aspects. This can for example be used to adapt the order in which content is shown to you, so that it is even easier for you to find (non-advertising) content that matches your interests.

Measure advertising performance 133 partners can use this purpose

Information regarding which advertising is presented to you and how you interact with it can be used to determine how well an advert has worked for you or other users and whether the goals of the advertising were reached. For instance, whether you saw an ad, whether you clicked on it, whether it led you to buy a product or visit a website, etc. This is very helpful to understand the relevance of advertising campaigns.

Measure content performance 59 partners can use this purpose

Information regarding which content is presented to you and how you interact with it can be used to determine whether the (non-advertising) content e.g. reached its intended audience and matched your interests. For instance, whether you read an article, watch a video, listen to a podcast or look at a product description, how long you spent on this service and the web pages you visit etc. This is very helpful to understand the relevance of (non-advertising) content that is shown to you.

Understand audiences through statistics or combinations of data from different sources 74 partners can use this purpose

Reports can be generated based on the combination of data sets (like user profiles, statistics, market research, analytics data) regarding your interactions and those of other users with advertising or (non-advertising) content to identify common characteristics (for instance, to determine which target audiences are more receptive to an ad campaign or to certain contents).

Develop and improve services 83 partners can use this purpose

Information about your activity on this service, such as your interaction with ads or content, can be very helpful to improve products and services and to build new products and services based on user interactions, the type of audience, etc. This specific purpose does not include the development or improvement of user profiles and identifiers.

Use limited data to select content 37 partners can use this purpose

Content presented to you on this service can be based on limited data, such as the website or app you are using, your non-precise location, your device type, or which content you are (or have been) interacting with (for example, to limit the number of times a video or an article is presented to you).

Use precise geolocation data 46 partners can use this special feature

With your acceptance, your precise location (within a radius of less than 500 metres) may be used in support of the purposes explained in this notice.

Actively scan device characteristics for identification 27 partners can use this special feature

With your acceptance, certain characteristics specific to your device might be requested and used to distinguish it from other devices (such as the installed fonts or plugins, the resolution of your screen) in support of the purposes explained in this notice.

Ensure security, prevent and detect fraud, and fix errors 92 partners can use this special purpose

Always Active

Your data can be used to monitor for and prevent unusual and possibly fraudulent activity (for example, regarding advertising, ad clicks by bots), and ensure systems and processes work properly and securely. It can also be used to correct any problems you, the publisher or the advertiser may encounter in the delivery of content and ads and in your interaction with them.

Deliver and present advertising and content 99 partners can use this special purpose

Always Active

Certain information (like an IP address or device capabilities) is used to ensure the technical compatibility of the content or advertising, and to facilitate the transmission of the content or ad to your device.

Match and combine data from other data sources 72 partners can use this feature

Always Active

Information about your activity on this service may be matched and combined with other information relating to you and originating from various sources (for instance your activity on a separate online service, your use of a loyalty card in-store, or your answers to a survey), in support of the purposes explained in this notice.

Link different devices 53 partners can use this feature

Always Active

In support of the purposes explained in this notice, your device might be considered as likely linked to other devices that belong to you or your household (for instance because you are logged in to the same service on both your phone and your computer, or because you may use the same Internet connection on both devices).

Identify devices based on information transmitted automatically 88 partners can use this feature

Always Active

Your device might be distinguished from other devices based on information it automatically sends when accessing the Internet (for instance, the IP address of your Internet connection or the type of browser you are using) in support of the purposes exposed in this notice.

Save and communicate privacy choices 69 partners can use this special purpose

Always Active

The choices you make regarding the purposes and entities listed in this notice are saved and made available to those entities in the form of digital signals (such as a string of characters). This is necessary in order to enable both this service and those entities to respect such choices.

have your say