Support from readers like you keeps The Journal open.

You are visiting us because we have something you value. Independent, unbiased news that tells the truth. Advertising revenue goes some way to support our mission, but this year it has not been enough.

If you've seen value in our reporting, please contribute what you can, so we can continue to produce accurate and meaningful journalism. For everyone who needs it.

IT IS HUGELY ironic that President Sarkozy called last week for Ireland’s corporate tax rate to be increased, as some sort of quid pro quo of the EU-IMF loan to Ireland. It is ironic, because it completely misses the point of who’s doing who a favour. Let’s leave aside, for the moment, the fact that the rate is a huge revenue raiser, that such things are a sovereign right and that Ireland is not being picked on for its low rate but for the fact that its rate is clear. (Other countries in the EU have effective rates than go lower than Ireland’s, depending on the FDI deal being dangled.)

One could certainly understand Mr. Sarkozy’s pronouncements if France and the other EU member states were gifting Ireland a large amount of money – some give and take would be expected. But what has happened is something designed to be a win-win for France, Germany and other EU states. Not only do their banks – the bondholders of the Irish banks – get off scot-free, while Irish taxpayers foot the bill, they as European governments earn a tidy little profit from the interest rate differential, middlemen between the markets and Ireland. In that context, the irony is the general perception that European taxpayers are helping to bailout Irish banks, while it is in fact Irish taxpayers helping to bailout European banks.

The “I Didn’t Do It” School of Thought

The Great Financial Crisis has given birth to two excuses: “I didn’t know what I was borrowing” and “I didn’t know what I was lending”. Ultimately, both cannot be true: in an economy with the rule of law, if neither the borrower nor the lender is responsible for their actions, something has gone wrong. So we know that at least one and possibly both of those arguments has to fall.

As more and more homes go “under water” into negative equity, it is easy to feel sympathy for the argument “I didn’t know what I was borrowing”. Given that they are the professionals, banks have at least in some sense a duty of care entering into a transaction, in the same way a doctor or solicitor has. This is in fact the thinking behind newbeginning.ie, which has been founded to help people who were clearly failed in the duty of care they were owed.

However, it’s not as simple as that. There were certainly, for example, public servants who felt as though they were forced into buying a two-bedroom apartment 80 miles from Dublin because they thought they’d never own their own home. But there were others who, looking around and seeing construction workers take home €100,000 a year, thought the whole thing was madness and avoided buying till it all blew over. A bank’s duty of care can be a convenient cloak under which to hide an abdication of personal responsibility.

What about the lenders to the Irish banks, the bondholders? The first rule of lending is that there is some risk of not being paid back in full. Despite this, the bondholders’ argument, when it has surfaced, has been that money was lent in good faith and borrowers were trusted to only take as much as they could manage sustainably. This is the “I didn’t know what I was lending” argument: why should they – as lenders – have to take a hit due to someone else’s mistake?

This only makes sense if Irish borrowers were so irresponsible as to undermine any responsibility the lenders had. Indeed, given that wealth is often destroyed and lenders have to take a hit, they would have to be so wilfully irresponsible that the Irish taxpayer had to step in to plug the holes created.

Advertisement

The Folly of the Irish?

So perhaps Irish households were silly? Perhaps they were so silly that not only does the “I didn’t know what I was borrowing” argument not stack up, but we can actually give 100% credence to the “I didn’t know what I was lending” argument by bondholders to Irish banks – i.e. European and US banks – and let them off on their merry way unharmed.

It’s pretty clear from even a cursory glance at the statistics that while Irish households may have been silly, Irish households were no more in the thrall of credit than other “more qualified” sectors of Irish society. The business sector in Ireland – people with business plans, shareholders and financial advisors – borrowed almost penny for penny the same amount as households did: while outstanding debt for households in Ireland rose from €57bn in 2003 to €153bn in late 2007, business debt rose from €47bn to €157bn in the same period. So, it’s clear from the statistics that it was not just Irish households.

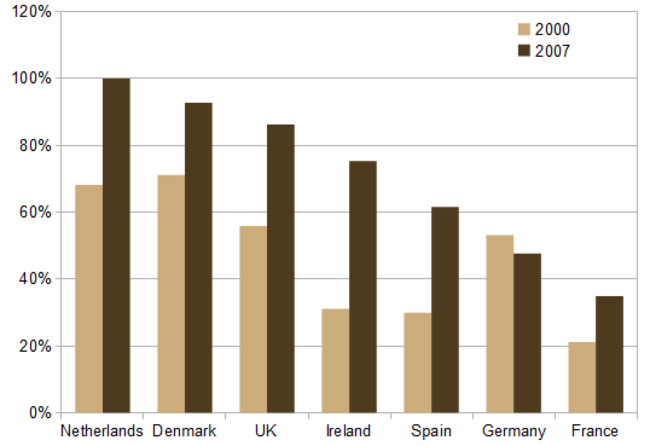

Not only that, Irish households were no more in the thrall of credit than households in other countries. For example, as the graph below shows, in 2007, residential mortgage debt in Ireland was 75% of GDP, compared to 85% or more in the UK, Denmark and the Netherlands. Instead, Ireland must be viewed as a microcosm – perhaps an extreme one, but one nonetheless – of the global financial environment over the last ten years. As all bubbles eventually do, the seemingly unending flow of money made it harder and harder to ignore the allure of cheap credit.

Mortgage debt, as percentage of GDP, selected countries (Source: Hypostat)

The Meat of the Sandwich

Irish banks – now owned by the Irish taxpayer – are in the middle of a sandwich. On the one hand, they have Irish households saying: “I didn’t know what I was borrowing.” On the other hand, they have international bondholders saying: “I didn’t know what I was lending.” Of course, Irish banks themselves could have tried to use either of those excuses up or down the line… but everyone knows that Irish banks have got to live with the consequences of their actions.

So will Irish households: the vast majority of Ireland’s mortgage debt will have to be – and will be – repaid. So this all comes down to whether anyone honestly believes 100% in the argument “I didn’t know what I was lending” on the part of bondholders – whether anyone honestly believes that while Irish banks and Irish households have to live with the consequences of their actions, international bondholders don’t.

This is not a call for default in knee-jerk reaction to austerity. Ireland needs austerity to bring its public finances back into line. The Irish Exchequer lived for many years precariously and in recent years well beyond its means and that is something all major political parties are committed to resolving in the coming years. The Irish taxpayer has to live with the consequences of its actions.

I am just about old enough to remember ads in the Irish newspapers in the 1980s with 17% interest rates. With all that’s happened in the last generation, it can be easy to forget that Ireland is not a country used to low interest rates. When it got them, for better or for worse, it assumed that plain sailing and easy credit was what it was like to be in a low and stable interest rate environment. Ireland got it wrong and will have to its price. And so did – and should – the people who lent to Ireland.

Readers like you are keeping these stories free for everyone...

A mix of advertising and supporting contributions helps keep paywalls away from valuable information like this article.

Over 5,000 readers like you have already stepped up and support us with a monthly payment or a once-off donation.

Red Cross says Gaza hospitals 'overwhelmed' after Israeli strikes kill more than 400 people

Updated

1 hr ago

32.6k

Garda Operation

Over 210 motorists arrested for driving under the influence during St. Patrick's weekend

5 mins ago

179

2

Analysis

A call to action in St Patrick's Cathedral today hit home hard after scenes in the White House

Christina Finn

Reports from New York

18 hrs ago

88.0k

236

Your Cookies. Your Choice.

Cookies help provide our news service while also enabling the advertising needed to fund this work.

We categorise cookies as Necessary, Performance (used to analyse the site performance) and Targeting (used to target advertising which helps us keep this service free).

We and our 157 partners store and access personal data, like browsing data or unique identifiers, on your device. Selecting Accept All enables tracking technologies to support the purposes shown under we and our partners process data to provide. If trackers are disabled, some content and ads you see may not be as relevant to you. You can resurface this menu to change your choices or withdraw consent at any time by clicking the Cookie Preferences link on the bottom of the webpage .Your choices will have effect within our Website. For more details, refer to our Privacy Policy.

We and our vendors process data for the following purposes:

Use precise geolocation data. Actively scan device characteristics for identification. Store and/or access information on a device. Personalised advertising and content, advertising and content measurement, audience research and services development.

Cookies Preference Centre

We process your data to deliver content or advertisements and measure the delivery of such content or advertisements to extract insights about our website. We share this information with our partners on the basis of consent. You may exercise your right to consent, based on a specific purpose below or at a partner level in the link under each purpose. Some vendors may process your data based on their legitimate interests, which does not require your consent. You cannot object to tracking technologies placed to ensure security, prevent fraud, fix errors, or deliver and present advertising and content, and precise geolocation data and active scanning of device characteristics for identification may be used to support this purpose. This exception does not apply to targeted advertising. These choices will be signaled to our vendors participating in the Transparency and Consent Framework.

Manage Consent Preferences

Necessary Cookies

Always Active

These cookies are necessary for the website to function and cannot be switched off in our systems. They are usually only set in response to actions made by you which amount to a request for services, such as setting your privacy preferences, logging in or filling in forms. You can set your browser to block or alert you about these cookies, but some parts of the site will not then work.

Targeting Cookies

These cookies may be set through our site by our advertising partners. They may be used by those companies to build a profile of your interests and show you relevant adverts on other sites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies, you will experience less targeted advertising.

Functional Cookies

These cookies enable the website to provide enhanced functionality and personalisation. They may be set by us or by third party providers whose services we have added to our pages. If you do not allow these cookies then these services may not function properly.

Performance Cookies

These cookies allow us to count visits and traffic sources so we can measure and improve the performance of our site. They help us to know which pages are the most and least popular and see how visitors move around the site. All information these cookies collect is aggregated and therefore anonymous. If you do not allow these cookies we will not be able to monitor our performance.

Store and/or access information on a device 109 partners can use this purpose

Cookies, device or similar online identifiers (e.g. login-based identifiers, randomly assigned identifiers, network based identifiers) together with other information (e.g. browser type and information, language, screen size, supported technologies etc.) can be stored or read on your device to recognise it each time it connects to an app or to a website, for one or several of the purposes presented here.

Personalised advertising and content, advertising and content measurement, audience research and services development 141 partners can use this purpose

Use limited data to select advertising 111 partners can use this purpose

Advertising presented to you on this service can be based on limited data, such as the website or app you are using, your non-precise location, your device type or which content you are (or have been) interacting with (for example, to limit the number of times an ad is presented to you).

Create profiles for personalised advertising 83 partners can use this purpose

Information about your activity on this service (such as forms you submit, content you look at) can be stored and combined with other information about you (for example, information from your previous activity on this service and other websites or apps) or similar users. This is then used to build or improve a profile about you (that might include possible interests and personal aspects). Your profile can be used (also later) to present advertising that appears more relevant based on your possible interests by this and other entities.

Use profiles to select personalised advertising 83 partners can use this purpose

Advertising presented to you on this service can be based on your advertising profiles, which can reflect your activity on this service or other websites or apps (like the forms you submit, content you look at), possible interests and personal aspects.

Create profiles to personalise content 38 partners can use this purpose

Information about your activity on this service (for instance, forms you submit, non-advertising content you look at) can be stored and combined with other information about you (such as your previous activity on this service or other websites or apps) or similar users. This is then used to build or improve a profile about you (which might for example include possible interests and personal aspects). Your profile can be used (also later) to present content that appears more relevant based on your possible interests, such as by adapting the order in which content is shown to you, so that it is even easier for you to find content that matches your interests.

Use profiles to select personalised content 34 partners can use this purpose

Content presented to you on this service can be based on your content personalisation profiles, which can reflect your activity on this or other services (for instance, the forms you submit, content you look at), possible interests and personal aspects. This can for example be used to adapt the order in which content is shown to you, so that it is even easier for you to find (non-advertising) content that matches your interests.

Measure advertising performance 132 partners can use this purpose

Information regarding which advertising is presented to you and how you interact with it can be used to determine how well an advert has worked for you or other users and whether the goals of the advertising were reached. For instance, whether you saw an ad, whether you clicked on it, whether it led you to buy a product or visit a website, etc. This is very helpful to understand the relevance of advertising campaigns.

Measure content performance 60 partners can use this purpose

Information regarding which content is presented to you and how you interact with it can be used to determine whether the (non-advertising) content e.g. reached its intended audience and matched your interests. For instance, whether you read an article, watch a video, listen to a podcast or look at a product description, how long you spent on this service and the web pages you visit etc. This is very helpful to understand the relevance of (non-advertising) content that is shown to you.

Understand audiences through statistics or combinations of data from different sources 74 partners can use this purpose

Reports can be generated based on the combination of data sets (like user profiles, statistics, market research, analytics data) regarding your interactions and those of other users with advertising or (non-advertising) content to identify common characteristics (for instance, to determine which target audiences are more receptive to an ad campaign or to certain contents).

Develop and improve services 83 partners can use this purpose

Information about your activity on this service, such as your interaction with ads or content, can be very helpful to improve products and services and to build new products and services based on user interactions, the type of audience, etc. This specific purpose does not include the development or improvement of user profiles and identifiers.

Use limited data to select content 38 partners can use this purpose

Content presented to you on this service can be based on limited data, such as the website or app you are using, your non-precise location, your device type, or which content you are (or have been) interacting with (for example, to limit the number of times a video or an article is presented to you).

Use precise geolocation data 46 partners can use this special feature

With your acceptance, your precise location (within a radius of less than 500 metres) may be used in support of the purposes explained in this notice.

Actively scan device characteristics for identification 27 partners can use this special feature

With your acceptance, certain characteristics specific to your device might be requested and used to distinguish it from other devices (such as the installed fonts or plugins, the resolution of your screen) in support of the purposes explained in this notice.

Ensure security, prevent and detect fraud, and fix errors 90 partners can use this special purpose

Always Active

Your data can be used to monitor for and prevent unusual and possibly fraudulent activity (for example, regarding advertising, ad clicks by bots), and ensure systems and processes work properly and securely. It can also be used to correct any problems you, the publisher or the advertiser may encounter in the delivery of content and ads and in your interaction with them.

Deliver and present advertising and content 97 partners can use this special purpose

Always Active

Certain information (like an IP address or device capabilities) is used to ensure the technical compatibility of the content or advertising, and to facilitate the transmission of the content or ad to your device.

Match and combine data from other data sources 72 partners can use this feature

Always Active

Information about your activity on this service may be matched and combined with other information relating to you and originating from various sources (for instance your activity on a separate online service, your use of a loyalty card in-store, or your answers to a survey), in support of the purposes explained in this notice.

Link different devices 53 partners can use this feature

Always Active

In support of the purposes explained in this notice, your device might be considered as likely linked to other devices that belong to you or your household (for instance because you are logged in to the same service on both your phone and your computer, or because you may use the same Internet connection on both devices).

Identify devices based on information transmitted automatically 86 partners can use this feature

Always Active

Your device might be distinguished from other devices based on information it automatically sends when accessing the Internet (for instance, the IP address of your Internet connection or the type of browser you are using) in support of the purposes exposed in this notice.

Save and communicate privacy choices 68 partners can use this special purpose

Always Active

The choices you make regarding the purposes and entities listed in this notice are saved and made available to those entities in the form of digital signals (such as a string of characters). This is necessary in order to enable both this service and those entities to respect such choices.

have your say